Why Your Audio Gear Needs More Than Hope and Prayers

As a musician, producer, or audio engineer, you know your equipment is more than just a collection of tools. Every microphone, console, and cable is an essential part of your creative process and, for many, the foundation of your career. Simply hoping for the best is a risky way to protect what is often a massive financial investment. Standard insurance like a homeowner's or renter's policy often sees your professional setup the same way it sees your sofa—and that's a problem. These policies just aren't built to handle the specific risks and high value of audio gear.

Let's paint a picture: a fire breaks out in your home studio. You lose $50,000 in carefully chosen equipment—vintage preamps, your DAW, and a collection of prized microphones. When you go to file a claim with your homeowner's insurance, the reality hits hard. Your policy has a small sub-limit of only $2,500 for business property. This leaves you with a devastating $47,500 loss and the overwhelming challenge of rebuilding your studio from the ground up. This isn't just a scary story; it's a common nightmare for creatives who don't realize their standard policy isn't a real safety net.

The Problem with One-Size-Fits-All Insurance

The main issue is that homeowner’s policies are designed for personal items, not the tools of your trade. They usually have serious blind spots when it comes to audio equipment:

- Business Use Exclusion: If you make any money from your music—whether through live gigs, studio sessions, or selling beats online—an insurer might reject your claim. They can argue the gear was used for business, which their policy doesn't cover.

- Low Coverage Limits: As the fire scenario shows, these policies put very low caps on what they'll pay for categories like electronics or business property. These limits are almost always far below the actual value of a professional audio setup.

- Actual Cash Value vs. Replacement Cost: Many standard policies pay out the Actual Cash Value (ACV), which factors in depreciation. That means you get what your five-year-old mixing console is worth today, not the $10,000 you would need to buy a new one.

This kind of professional audio equipment requires specialized coverage.

The complex and high-value nature of this gear is exactly why a generic policy can't provide the financial protection you truly need.

The complex and high-value nature of this gear is exactly why a generic policy can't provide the financial protection you truly need.

A Growing Market Means Growing Risk

The total value of gear in studios and on tour is enormous. The global audio equipment market was valued at around $66.62 billion in 2024 and is expected to keep growing as technology improves. This trend means the cost to replace your equipment is always on the rise, making the gap between its value and what a standard policy covers even wider.

Specialized audio equipment insurance is made to fill this gap. It's built for the world you work in—covering everything from a dropped microphone at a gig to a power surge that fries your entire rack. As you grow your gear collection, maybe by finding good deals on pre-owned items, remember that every new piece adds to your total risk. To learn more about sourcing gear smartly, you can review our guide on buying used audio equipment. Getting the right insurance isn't just another expense; it’s an essential protection for your career.

Decoding Coverage Types That Actually Protect Your Investment

Diving into the world of audio equipment insurance can feel like trying to mix a track with all the labels in a different language. It's easy to get lost in the terms and fine print. But getting a handle on the main types of coverage is critical, because not all policies are the same. Proper protection isn't just about being insured; it's about having the right insurance for your gear, whether it's safe in your studio or getting tossed onto a tour bus.

Think of your insurance policy as a custom-built road case for your finances. A basic homeowner's policy is like a flimsy gig bag—it offers minimal protection. For professional work, you need something far more robust. The first choice you'll often face is between Replacement Cost Value (RCV) and Actual Cash Value (ACV) coverage. ACV pays for the current, depreciated value of your gear. So if your five-year-old console is destroyed, you'll only get a fraction of its original price.

RCV, however, provides enough money to buy a brand new, similar item. This gets you back in business without having to dig deep into your own pocket. For anyone whose gear is essential for their income, RCV is almost always the smarter choice.

Key Coverage Areas to Consider

Beyond how your gear's value is calculated, a solid policy must shield you from the specific risks you face daily. A home studio producer's needs are very different from a live sound engineer's. The best audio equipment insurance policies let you pick and choose what you need.

- Accidental Damage: This covers the "oops" moments—a dropped microphone, a spilled coffee on your mixer, or a power surge that toasts your preamps. It's a must-have for any gear that sees regular use.

- Theft: This protects your equipment from being stolen, whether it's from your studio, your car, or backstage at a venue. With the high value and portability of audio gear, this is non-negotiable.

- In-Transit and Touring Coverage: If your gear ever leaves your main location, you need this. It covers your equipment while it's being moved to gigs, festivals, or recording sessions. Many standard policies won't cover your gear once it's off the premises. You can see many kinds of mobile-friendly audio equipment categories on Gearsupply that are common in touring rigs.

- Liability Coverage: This is absolutely essential for anyone working live events. If a speaker you set up falls and injures an audience member, liability coverage can save you from financially devastating legal and medical bills.

To help you see how these different coverages stack up, here is a breakdown of what each one typically includes and who it's designed for.

Audio Equipment Insurance Coverage Comparison

A detailed comparison of different coverage types, what they protect against, and typical cost ranges

| Coverage Type | Protection Level | What's Covered | Best For | Typical Cost Range |

|---|---|---|---|---|

| Accidental Damage | High | Drops, spills, power surges, and other unforeseen physical mishaps. | All active musicians, producers, and engineers. | $10 - $30 per month |

| Theft | High | Gear stolen from your studio, vehicle, venue, or storage unit. | Anyone with portable or high-value equipment. | $15 - $40 per month |

| In-Transit / Touring | Specialized | Protection against damage or theft while traveling to and from gigs. | Touring musicians, mobile DJs, and live sound companies. | $20 - $50+ per month |

| General Liability | Essential | Bodily injury or property damage caused by your equipment or setup. | Live event professionals, venue owners, and rental houses. | $25 - $75+ per month |

| Replacement Cost (RCV) | High | Provides funds to buy a new equivalent replacement for damaged/stolen gear. | Professionals who rely on their gear for income. | Added to base policy cost |

| Actual Cash Value (ACV) | Basic | Pays the current market value (original cost minus depreciation) of your gear. | Hobbyists or those with older, less critical equipment. | Standard in basic policies |

This comparison shows that a truly protective policy is built in layers. While accidental damage and theft are common, specialized coverage like in-transit and liability address the unique risks of the audio world.

The data clearly shows that while accidents are frequent, the claims can be substantial. An average payout of $2,500 underscores why having strong coverage is more than just a good idea—it's a crucial business decision. By understanding these options, you can build a policy that secures your creative tools and protects your livelihood.

High-End Gear Needs High-Level Protection Strategies

When your audio setup evolves from a passion into a professional or collector's investment, the way you protect it must also change. A standard insurance policy is like using a dust cover in a hurricane—it's just not built for that level of risk. High-end equipment, like vintage mixing consoles or custom monitor systems, has unique risks that basic policies don't cover, potentially leaving six-figure setups dangerously exposed.

This isn't a small niche; it's a significant and expanding market. The premium audio sector was valued at around $11.65 billion in 2024 and is expected to climb to $32.47 billion by 2033. This growth shows a clear trend toward investing in more valuable gear, which means the need for strong audio equipment insurance is more critical than ever. As the value of your equipment rises, so does the potential financial hit from theft, damage, or disaster. Recent industry reports offer more insight into the impressive growth of the premium audio market.

Valuing the Irreplaceable: Custom and Vintage Gear

Protecting high-end gear means going beyond a simple list of serial numbers. The main difficulty is correctly valuing items that you can't just buy again off the shelf.

Appreciating Assets: Unlike most electronics that lose value, some vintage equipment, such as a classic Neumann U 47 microphone or a Fairchild 670 compressor, can actually increase in value over time. Standard policies that calculate value based on depreciation will severely underinsure these pieces. A specialized policy should use an agreed value, which is set by a professional appraisal, to make sure you get compensated for its true market worth.

Custom Modifications: Many audio pros tweak their gear for better performance. These upgrades add a lot of value but are often overlooked by standard insurers who only see the stock model. Keeping detailed records of every modification, including receipts and photos, is essential to prove its increased value.

One-of-a-Kind Pieces: For custom-built consoles or rare prototypes, replacement is impossible. The insurance strategy here isn't about replacement cost but about covering the financial blow of losing a unique and essential creative tool.

Building a Fort Knox of Protection

Properly insuring your high-end equipment involves more than just a policy; it's a complete protection plan. This plan should include thorough documentation like professional appraisals, high-resolution photos, and a detailed inventory that you update every year. For a good start on managing your gear, our guide on sound system basics can be quite useful.

For valuable gear, physical care is just as important as financial protection. Following a regular maintenance schedule, similar to using proactive equipment maintenance checklists, can extend the life of your equipment and may even lower your number of claims. By pairing a specialized insurance policy with careful documentation and maintenance, you can ensure your most valuable assets are truly safe, protecting both their financial and creative worth.

What You're Really Paying For Beyond The Premium Quote

When an insurance quote lands in your inbox, it's natural to fixate on the monthly premium. That’s the number you see leaving your bank account, after all. But that premium is just the surface. What you're actually buying is a financial safety net, and its cost is calculated based on a range of factors that paint a picture of your specific risk. Insurers are essentially figuring out the likelihood of you filing a claim, and that calculation directly sets your premium.

Figuring out what drives these costs is the first step toward getting the right coverage without overspending. It's not just about the total value of your gear, though that’s a big piece of the puzzle. The true cost of audio equipment insurance is shaped by how, where, and how often you use your expensive equipment. A bedroom producer whose gear never leaves the house is a much lower risk than a touring musician whose equipment is constantly being moved, handled by various crews, and used in different venues. This difference in risk exposure is what makes one premium higher than another.

Unpacking the Core Cost Factors

Several key elements work together to determine your final quote. Think of it like mixing a track—each element has its own fader, and adjusting one can affect the entire balance. The goal is to find that sweet spot where you have solid protection that fits your budget.

Your insurance premium is influenced by a number of variables. The table below breaks down the main cost drivers, showing how much they can affect your premium and what you can do to manage them.

| Cost Factor | Impact Level | Typical Range | Optimization Strategy | Potential Savings |

|---|---|---|---|---|

| Equipment Value | High | $5 - $15 per $1,000 of value | Maintain an accurate inventory; remove items you no longer own. | 5-10% |

| Usage Patterns | High | Premiums can be 30-50% higher for touring vs. studio use. | Be specific about usage. If you only tour occasionally, seek a policy that reflects that. | 15-25% |

| Geographic Location | Medium | 10-20% variance based on local crime rates. | If possible, store gear in a lower-risk area; highlight secure storage in your application. | 5-15% |

| Security Measures | Medium | Discounts can reach 5-15%. | Install and document security systems, secure locks, and climate controls. | 5-15% |

| Deductible Amount | High | A $1,000 deductible can lower premiums by 20-40% vs. a $250 deductible. | Choose the highest deductible you can comfortably afford to pay out-of-pocket. | 20-40% |

| Claims History | Medium | A clean record can result in a 5-10% "no-claim" discount. | Implement strong risk management practices to prevent claims. | 5-10% |

As the table shows, factors like your gear's value and how you use it have a high impact, but you have significant control over the final cost through your deductible choice and security measures.

Strategies for Balancing Cost and Coverage

Getting the best value from your insurance isn't about finding the cheapest plan, but the smartest one. You can actively manage your premium by making strategic choices. One of the most powerful tools at your disposal is the deductible—the amount you pay out-of-pocket on a claim before your insurance coverage starts.

Opting for a higher deductible usually leads to a lower monthly premium. If you have the savings to comfortably cover a $1,000 deductible in case of an incident, you could see a major drop in your yearly insurance costs compared to a policy with a $250 deductible. If you decide to upgrade or downsize your setup, knowing what your gear is worth on the open market is also useful. Our guide on where to sell used audio equipment can provide helpful information. By thoughtfully considering these factors, you can build a policy that gives you peace of mind at a price that works for you.

Choosing The Right Policy Without Getting Burned

Picking the right audio equipment insurance policy feels a lot like a final mixdown. Every small adjustment matters, and one wrong move can throw off the entire project. This isn't just about finding the lowest monthly payment; it's about taking a hard look at your real-world risks and finding coverage that matches how you actually work. The key is a methodical approach, starting with a clear picture of what you own and how you use it.

Smart studios and touring professionals don't leave this to chance. They start with a detailed equipment inventory, noting every single microphone, cable, and software license. This list is more than just a personal record; it's the foundation for any insurer. By creating this inventory, you establish a clear, documented value for your gear. This makes the quote process faster and more accurate, and it gives you essential proof if you ever need to file a claim. You can easily find checklists and inventory templates online to help you get started.

Reading Between the Lines of Your Policy

With your inventory complete, it's time to dive into the policy documents. An insurance policy is a legal contract, and the devil is in the details hidden in the fine print. To make a smart choice and protect your assets, it helps to approach it with the same care as any other formal agreement. Adopting good contract management best practices can shift your mindset from simply buying a product to entering into a serious partnership.

Pay close attention to these key areas:

- Exclusions: What does the policy specifically not cover? It's common to see exclusions for damage from mold, building-wide electrical problems, or gear left in an unlocked vehicle.

- Coverage Limits: Are there separate, lower limits for certain items? A $50,000 policy might only cover up to $5,000 for laptops or other portable electronics.

- Conditions for Coverage: What are your obligations? For instance, a policy might demand a monitored alarm system at your studio for theft coverage to apply.

Overlooking these details is a frequent and expensive mistake. You’ll hear stories from industry veterans about claims being denied because a specific condition—like storing gear in a certified locked case—wasn't followed. These aren't just suggestions; they are the binding rules of your coverage.

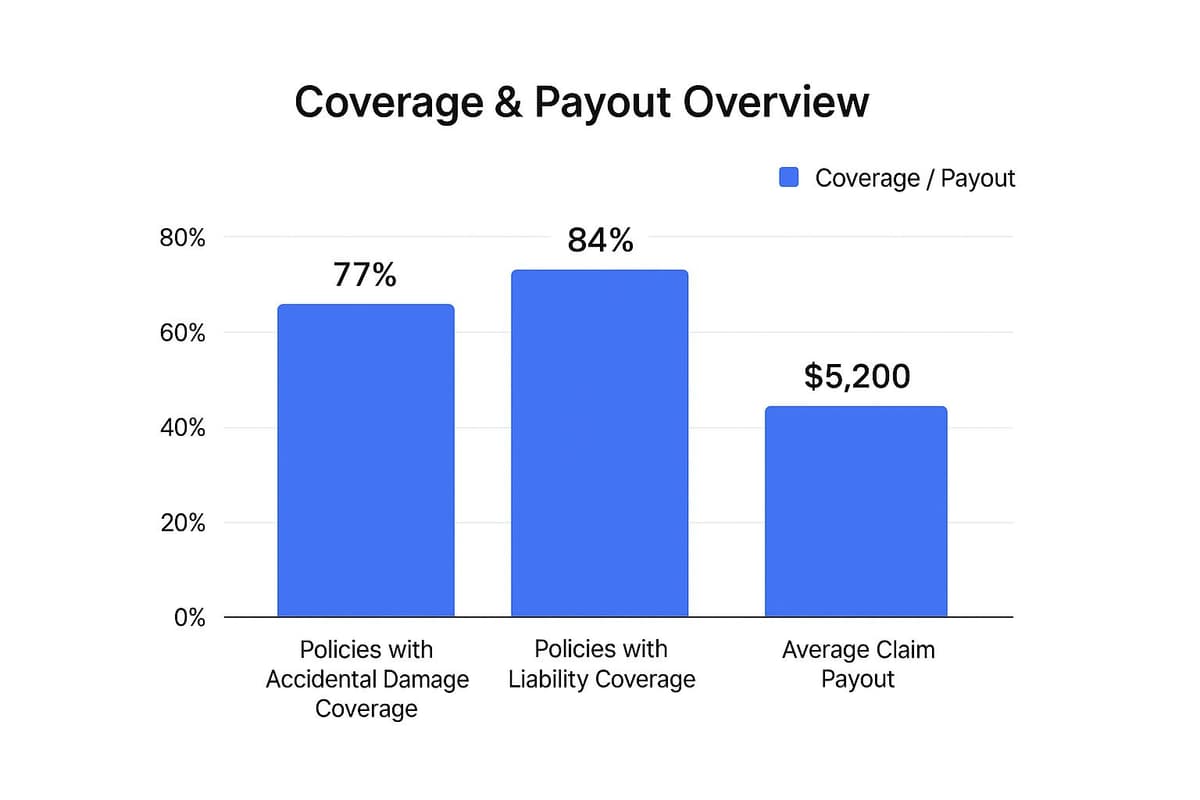

Framework for Evaluating Insurers and Policies

Not every insurance company understands the specific world of audio professionals. It's important to find a provider who speaks your language and gets what you do.

This image shows that insurance isn't a one-size-fits-all product. Finding a company with experience in the creative or live events industry is essential for getting the right kind of protection. When you compare providers, ask questions that cut through the marketing noise. For example, ask how they determine the value of a rare piece of vintage gear you found in our marketplace listings or a custom-modified console. A fuzzy answer should be a major red flag.

Finally, create a simple comparison chart to weigh your top options side-by-side. List each provider and compare them on the most important factors: premium, deductible, touring coverage, accidental damage specifics, and their process for valuing your gear. This organized method helps you make a logical decision and clearly see which policy offers the best protection for your hard-earned equipment. You can also browse our Community Listings to get a sense of the current market value for common audio gear.

How the Digital Revolution Changes the Insurance Game

The world of audio production has seen a massive shift from old-school analog studios to interconnected digital setups. This is more than just swapping tape machines for recording software; it’s a total change in how we create, save, and use our gear and our projects. For anyone with a podcasting rig, a streaming setup, or a home studio linked to the internet, this new reality brings new dangers that older audio equipment insurance policies were never built to handle. The rules for protecting your gear are changing because the equipment itself—and how it can be compromised—has been completely reinvented.

Imagine an analog studio from the past as a physical fortress with one big, secure vault. Insuring it was simple: protect the expensive hardware locked inside. A modern digital studio, however, is more like a smart home with countless windows and doors. Every device connected to your network, from your digital mixer to a smart speaker you use for referencing tracks, is a potential way in for trouble. This web of connections creates risks that go far beyond a simple break-in or a dropped piece of gear.

The New Threats in a Connected World

Today's creative studio is a complex mix of hardware and software. A hybrid setup, which blends classic analog gear with digital interfaces and cloud services, is an especially tricky puzzle for insurance. Insurers now have to account for dangers that used to be the concern of IT professionals, not music producers or podcasters.

These new risks include:

- Cyber Attacks on Smart Systems: A hacker could get into your networked audio system. Instead of stealing your physical gear, they could push a malicious firmware update that turns your expensive equipment into a useless brick.

- Cloud-Based Workflow Risks: Many of us depend on cloud storage for project files and backups. If that service fails or your account gets hacked, you haven't lost a physical item, but you've lost priceless digital work. A standard equipment policy usually won't cover this kind of loss.

- Data Corruption and Software Failure: A critical software bug or corrupted project file can stop your work just as surely as a broken mixing board. The cost to recover that data and the income you lose while you're down is a new type of financial hit.

A Market Reshaped by Digital Demand

This digital shift is happening while the world of content creation is exploding. The global market for audio and video equipment was valued at a massive $308.39 billion in 2024, largely driven by the demand for podcasting gear, streaming setups, and home studio equipment. With internet access in the U.S. alone reaching nearly 94%, the number of connected devices—and the powerful audio gear they're linked to—is only going up.

This boom in high-tech equipment directly increases the need for specialized insurance that gets these modern risks. You can learn more about these market forces in this full research report. As our studios get smarter and more connected, the way we protect them has to evolve, too. We need to make sure our insurance policies cover our digital reality, not just our physical hardware.

Getting Paid When Disaster Strikes Your Setup

Having the right audio equipment insurance policy is a great start, but knowing how to file a claim is what actually turns that policy into a financial safety net. When something goes wrong—a theft, a fire, or a mishap on the road—your ability to recover quickly depends on how well you've prepared and how you handle the process. Think of it like this: your policy is the fire extinguisher, but knowing how to pull the pin and aim is what puts out the flames.

The entire claims process boils down to one critical thing: documentation. You have to prove what you lost and what it was worth. Insurance companies work with facts, not assumptions. Without solid proof, even the best policy can lead to a delayed, disputed, or denied claim. When trouble hits your audio setup, following the right steps is essential. For a general overview of filing an insurance claim and what to expect, you can check out helpful resources on understanding the insurance claims process.

Your Pre-Disaster Documentation Checklist

The work you do before an incident happens is what truly saves you. A detailed and organized inventory is your most powerful tool when you need to make a claim.

- Create a Master Inventory: Use a simple spreadsheet to list every piece of gear. Be sure to include the make, model, serial number, when you bought it, and how much it cost.

- Photograph Everything: Take clear, well-lit photos of each item. Get close-ups of serial numbers and any unique markings or custom modifications. Store these images safely in a cloud service.

- Keep Your Receipts: Whether digital or paper, every receipt is a piece of evidence. For valuable vintage gear, it's a good idea to get a professional appraisal every few years to have its current market value on record. An appraisal is a powerful, third-party valuation that’s hard for an adjuster to argue with.

Navigating the Claims Process Step-by-Step

When you have to file a claim, the key is to stay calm and be methodical. Your actions right after the loss can make a big difference in the final outcome.

- Contact Your Insurer Immediately: Report the loss as soon as it's safe to do so. Your provider will give you a claim number, assign an adjuster, and walk you through the next steps and required forms.

- Provide All Documentation: This is where your prep work pays off. Submit your detailed inventory, photos, receipts, and a copy of the police report if your gear was stolen. The more complete your initial submission is, the faster the process will go.

- Work with the Adjuster: The adjuster’s job is to verify your loss. They likely won't be an audio expert, so be ready to patiently explain what a piece of gear does and why it's valuable. Your detailed records are your best friend in this conversation.

- Review the Settlement Offer: Read the initial offer carefully. If it seems too low—especially if they've miscalculated depreciation on a replacement cost policy—don't hesitate to push back. Politely provide your evidence, like appraisals or listings for comparable gear. Sometimes, professional repair is a viable option; you can find tips on finding the right technician in our guide to pro audio repair.

By treating insurance as a core part of your professional strategy, you make sure that if the worst should happen, you're prepared to get paid what you're owed and get back to making music.

At Gearsupply, we know your equipment is your livelihood. While our marketplace helps you build your dream rig, protecting that investment is just as important. Secure your gear with reliable insurance so you're always ready for the next show.